The growth of the mobile money market is significantly driven by the increasing initiatives taken by governments globally to promote a cashless economy. The rising adoption of digital payment-based business models by organizations is a key contributing factor, fostering market expansion. The enhanced efficiency of mobile money transactions serves as a catalyst for the overall growth of the market, as streamlined digital payments can stimulate increased spending, prompting companies to invest in and advance this technology. Consequently, the surge in demand for mobile money payments is witnessed, further propelled by the escalating adoption of mobile point-of-sale solutions.

Among the pivotal factors boosting the market, the strategic move towards greater flexibility through mobile money for attracting businesses stands out, providing companies with versatile financial solutions. The proliferation of NFC-enabled handsets adds another dimension to the market’s evolution, facilitating seamless and secure mobile transactions. Additionally, the heightened focus on research and development activities within the mobile money market not only ensures ongoing innovation but also opens up new opportunities for growth in the forecast period. As businesses increasingly recognize the advantages of mobile money solutions, coupled with technological advancements and expanding infrastructure, the mobile money

Definition

The term “mobile money” refers to utilising your mobile devices to make financial transactions without needing actual currency. Remittances, bill payments, and airtime purchases are the main sources of funding for mobile banking services. These solutions facilitate the dual goals of giving service providers a chance and acting as a catalyst for financial inclusion.

Pros and cons of mobile money

Pros of Mobile Money:

- Financial Inclusion: Mobile money services have played a significant role in promoting financial inclusion by providing banking services to individuals who may not have access to traditional banking infrastructure.

- Convenience: Mobile money offers unparalleled convenience, allowing users to conduct financial transactions, pay bills, and transfer funds anytime, anywhere using their mobile devices.

- Reduced Transaction Costs: Compared to traditional banking methods, mobile money transactions often involve lower fees, making it a cost-effective solution, especially for small-value transactions.

- Speed of Transactions: Mobile money transactions are processed in real-time, providing quick and efficient financial transactions, which is crucial for various daily activities.

- Security Features: Mobile money services incorporate advanced security measures such as PIN codes and biometric authentication, ensuring the safety and integrity of financial transactions.

Cons of Mobile Money:

- Limited Infrastructure in Some Regions: In certain regions, especially in developing countries, the lack of robust telecommunications and internet infrastructure may limit access to mobile money services.

- Security Concerns: While mobile money services have security features, there is still a risk of unauthorized access, fraud, and other security breaches, particularly if users are not vigilant with their personal information.

- Dependence on Mobile Networks: Mobile money transactions are reliant on mobile network connectivity. Issues such as network outages or poor coverage can disrupt the accessibility and usability of mobile money services.

- Limited Merchant Acceptance: In some areas, the acceptance of mobile money payments may be limited, hindering users’ ability to use mobile money for various transactions, including purchases.

- Transaction Limits: Some mobile money services impose transaction limits, which can be a constraint for users requiring higher transaction volumes or larger amounts.

Growth in mobile money market

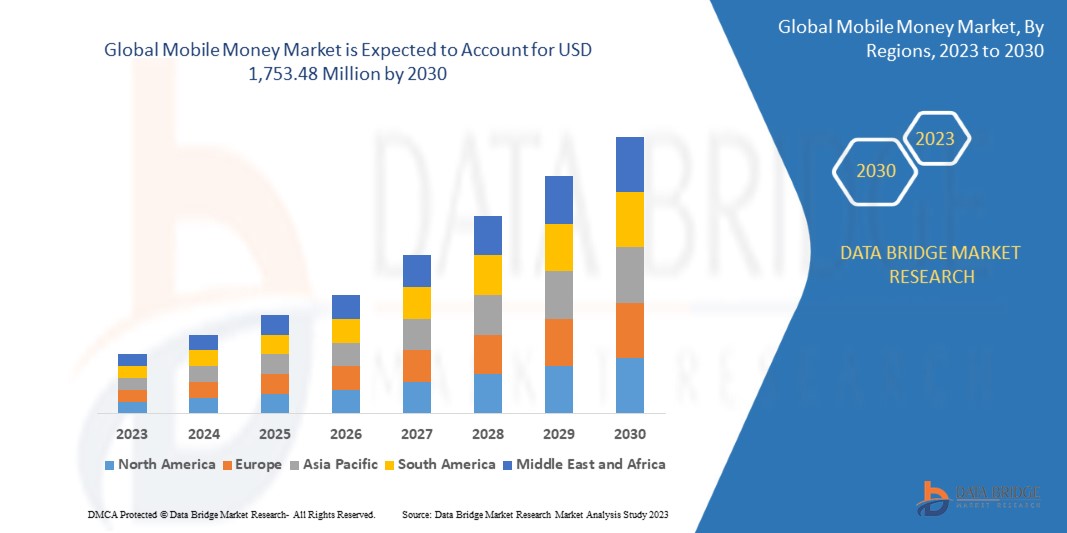

Data Bridge Market Research’s analysis reveals a dynamic trajectory for the global mobile money market, reflecting substantial growth and transformative trends. In 2022, the market recorded a valuation of USD 77.36 million, and projections indicate a remarkable ascent, reaching an estimated USD 1,753.48 million by 2030. This growth trajectory is anticipated to be driven by a robust Compound Annual Growth Rate (CAGR) of 34.4% during the forecast period from 2023 to 2030. Notably, within the industry vertical segment, Banking, Financial Services, and Insurance (BFSI) are poised to dominate in 2022. This dominance is attributed to the rapid digital transformation witnessed within the BFSI sector, showcasing the sector’s embrace of mobile money solutions.

The comprehensive market report by Data Bridge Market Research goes beyond conventional market metrics, providing an in-depth analysis. This includes expert insights, import/export dynamics, pricing trends, production-consumption patterns, and a thorough PESTLE analysis. As the global mobile money market undergoes this substantial growth, stakeholders can leverage the comprehensive insights provided by Data Bridge Market Research for strategic decision-making in a dynamic and evolving market landscape.

Role of Mobile Money in Financial Inclusion

The role of mobile money in financial inclusion is pivotal, playing a transformative role in expanding access to financial services for individuals who have traditionally been excluded from the formal banking sector. Several key aspects illustrate the significant contribution of mobile money to promoting financial inclusion:

- Accessibility: Mobile money services enable individuals to access basic financial services through their mobile phones, eliminating the need for physical bank branches. This is particularly crucial in regions with limited banking infrastructure.

- Reach to the Unbanked: Mobile money reaches populations that are unbanked or underbanked, including those in remote or rural areas where traditional banking services may be scarce or inaccessible.

- Affordability: Mobile money transactions often have lower costs compared to traditional banking services. This affordability is especially important for individuals with lower incomes who may be deterred by high fees associated with traditional banking.

- Microfinance and Small Transactions: Mobile money facilitates microfinance transactions and small-value transfers, allowing individuals to save, borrow, and make transactions of modest amounts, which may not be economically viable within traditional banking structures.

- Financial Education: Mobile money platforms often incorporate educational features, providing users with information on financial literacy, budgeting, and savings. This contributes to enhancing the financial knowledge and capabilities of users.

- Convenient Savings and Transactions: Mobile money allows individuals to save money securely and conduct various transactions, such as payments, transfers, and bill settlements, conveniently through their mobile devices.

- Mobile Money Agents: The network of mobile money agents, often local businesses or individuals, serves as touchpoints for users to convert cash into digital currency and vice versa. This decentralized approach enhances accessibility in remote areas.

For more such information about mobile money market visit

https://www.databridgemarketresearch.com/reports/global-mobile-money-market